All in one Banking-

All about banking just a click away.

Date: July 04,2026.

Premature redemption under Sovereign Gold Bond (SGB) Scheme - SGB 2020-21 Series-IX

Excerpts:

The next due date of premature redemption of the above tranche shall be on July 04, 2026 (July 05 being holiday).

The redemption price for premature redemption due on July 04, 2026, (July 05 being holiday) shall be ₹14,366/- (Rupees Fourteen Thousand Three Hundred and Sixty Six Only) per unit of SGB

Read More

Top / Back to Home Page.

Date: July 01,2026.

Premature redemption under Sovereign Gold Bond (SGB) Scheme - Redemption Price for premature redemption of SGB 2018-19 Series-IV due on July 01, 2026

Excerpts:

The next due date of premature redemption of the above tranche shall be on July 01, 2026.

The redemption price for premature redemption due on July 01, 2026, shall be ₹14,086/- (Rupees Fourteen Thousand and Eighty Six Only) per unit of SGB

Read More

Sovereign Gold Bond Scheme 2018-19.

(Since discontinued)

Top / Back to Home Page.

Date: June 28,2026.

DIKSHA: Powering India's Digital Learning Ecosystem

Excerpts:

Posted On: 28 JUN 2026 12:06PM by PIB Delhi

A National Platform for Education

Digital Infrastructure for Knowledge Sharing (DIKSHA) is an open-source platform that provides easy access to high-quality, curriculum-linked digital learning materials in multiple languages to students and teachers across the country. It is a key component of the PM e-Vidya initiative of the Ministry of Education that aims to ensure continuity of learning through online means.

DIKSHA can be customised to suit different needs and has therefore been widely accepted and adopted by various boards in almost all states and UTs

DIKSHA aims to create a dynamic learning ecosystem powered by technology and innovation.

It promotes accessible, engaging, and personalised experiences for diverse learner needs.

The platform features media-rich, interactive resources, including 2D/3D animations, AR experiences, simulations, virtual labs, and sign language videos, designed to enhance conceptual clarity and cater to diverse learning styles.

DIKSHA empowers personalised learning with unlimited practice questions, detailed solutions, adaptive assessments, and competency-based question banks that identify gaps and enable timely remediation.

This integrated ecosystem—combining content creation, curation, consumption, and analytics—drives inclusive, data-informed, and joyful learning aligned with NEP 2020.

Platform Structure and Content Verification

The DIKSHA platform is designed to ensure decentralised participation and rigorous content validation. Its structure enables contribution while maintaining quality standards through periodic review.

The platform operates on a federated architecture, enabling each participant to upload and manage content independently.

The Central Institute of Educational Technology (CIET-NCERT) periodically validates participant content based on prescribed guidelines.

DIKSHA platform supports both online and offline accessibility. Learners can download content in advance and access it conveniently without an active internet connection.

States and Union Territories preload content on Smart Class boards to ensure dependable offline access.

Excerpts:

Read More

Top / Back to Home Page.

Date: June 27,2026.

RBI issues Master Direction – Reserve Bank of India (Credit Derivatives) Directions, 2026

Excerpts:

Read More

Master Direction – Reserve Bank of India (Credit Derivatives) Directions, 2026

Excerpts:

Read More

RBI releases draft Master Direction - Reserve Bank of India (Call, Notice and Term Money Markets) Directions, 2026

Excerpts:

Read More

Master Direction- Reserve Bank of India (Call, Notice and Term Money Markets) Directions, 2026 - Draft

Excerpts:

Read More

RBI releases draft Master Direction – Reserve Bank of India (Secondary Market Transactions in Government Securities) Directions, 2026

Excerpts:

Read More

Master Direction - Reserve Bank of India (Secondary Market Transactions in Government Securities) Directions, 2026 – Draft

Excerpts:

Read More

RBI Issues Amendment Directions on ‘Review of Framework of Limiting Customer Liability in Digital Transactions’

Excerpts:

Read More

Reserve Bank of India (Commercial Banks - Responsible Business Conduct) Third Amendment Directions, 2026

Excerpts:

Read More

Top / Back to Home Page.

Date: June 21,2026.

RBI issuesed Circular on Lead Bank Scheme on June 19,2026

Excerpts:

Objective of Lead Bank Scheme

LBS aims at coordinating the activities of banks, government and other developmental agencies through fora established under the Scheme to achieve the following:

a) enhancing flow of credit to priority sectors for achieving inclusive growth.

b) deepening financial inclusion through improved access and usage of financial services.

Framework of the Scheme

Lead Bank:

i) RBI shall designate a commercial bank as Lead Bank in each district, to coordinate the efforts of the banks, Government, National Bank for Agriculture and Rural Development (NABARD) and other stakeholders at the district level to improve credit flow to the priority sectors and promote financial inclusion in the district.

ii) The list of district-wise Lead Banks is given in Annex-1.

Lead District Manager (LDM):

Every Lead Bank shall appoint a Lead District Manager (LDM) in each district where it has lead bank responsibility, to exclusively oversee and coordinate the implementation of LBS in the district.

District Development Manager (DDM):

NABARD shall appoint a District Development Manager (DDM) for each district to act as a liaison between NABARD and the district-level banking and financial institutions in promoting rural credit, implementing financial inclusion initiatives, and supporting agricultural and rural development activities in the district.

Lead District Officer (LDO):

RBI shall designate one of its officers as Lead District Officer (LDO) for each district. The LDO shall represent the Bank at the district level under the LBS.

SLBC Convenor Bank:

i) RBI shall designate one commercial bank with significant presence in the State / Union Territory (UT) as the State Level Bankers’ Committee (SLBC) Convenor Bank / UT Level Bankers’ Committee (UTLBC) Convenor Bank.

ii) List of State and UT-wise SLBC / UTLBC Convenor Banks is given in Annex-1.

SLBC Convenor:

SLBC Convenor bank in each State / UT shall designate a General Manager of the bank as the SLBC Convenor. In case no General Manager level official is available, the Zonal Head of the Convenor bank (not below rank of DGM) may be designated as Convenor.

Fora under the Lead Bank Scheme

The scheme shall function through a three-tier structure in each State / UT, with Block Level Bankers’ Committee (BLBC) at the base level, District Consultative Committee (DCC) and District Level Review Committee (DLRC) at the intermediate level, and SLBC / UTLBC at the apex level. Each of these fora shall broadly comprise of banks, government agencies and other stakeholders.

Block Level Bankers’ Committee (BLBC)

5.1 Purpose

BLBC shall be constituted in each block of a district for achieving coordination at the block level among banks, government and field level development agencies. BLBC shall prepare and review the implementation of the Block Credit Plan and resolve operational issues in the implementation of credit programmes at the block level.

Read More- Lead Bank Scheme revised RBI Circular

Top / Back to Home Page.

Date: June 21,2026.

Minutes of the Monetary Policy Committee Meeting, June 3 to 5, 2026

Excerpts:

MPC voted unanimously to keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 5.25 per cent.

The standing deposit facility (SDF) rate remains at 5.00 per cent and

The marginal standing facility (MSF) rate and the Bank Rate remain at 5.50 per cent.

The MPC also decided to continue with the neutral stance.

Read More

Top / Back to Home Page.

Date: June 17,2026.

RBI Issues Master Directions on Authorisation to operate a Payment System

Excerpts:

Today, RBI has issued Master Directions on Authorisation to operate a Payment System which consolidates instructions issued through following circulars/ guidelines, and comes into effect immediately:

Computation of Net-worth dated January 16, 2015.

Guidelines for Voluntary Surrender of Certificate of Authorisation dated May 12, 2016.

On-tap Authorisation of Payment Systems dated October 15, 2019.

Authorisation of entities for operating a Payment System under the PSS Act – Introduction of Cooling Period dated December 04, 2020.

Perpetual Validity for Certificate of Authorisation (CoA) issued to Payment System Operators dated December 04, 2020.

Investment in Entities from FATF Non-compliant Jurisdictions dated June 14, 2021.

Framework for Voluntary Surrender of Certificate of Authorisation dated May 12, 2023.

Read More.

Master Directions on Authorisation to operate a Payment System

Top / Back to Home Page.

Date: June 11,2026.

Premature redemption under Sovereign Gold Bond (SGB) Scheme - Redemption Price for premature redemption of SGB 2019-20 Series I

Excerpts:

The due date of premature redemption of the above tranche shall be on June 11, 2026.

The redemption price for premature redemption due on June 11, 2026, shall be ₹15,038/- (Rupees Fifteen Thousand and Thirty Eight only) per unit of SGB

Read More

Top / Back to Home Page.

Date: June 08,2026.

Premature redemption under Sovereign Gold Bond (SGB) Scheme - Redemption Price for premature redemption of SGB 2021-22 Series-III

Excerpts:

The due date of premature redemption of the above tranche shall be on June 08, 2026.

The redemption price for premature redemption due on June 08, 2026, shall be ₹15,512/- (Rupees Fifteen Thousand Five Hundred and Twelve only) per unit of SGB

Read More.

Note: The issue price of the above SGB was Rs 4,889 per unit of SGB.A further reduction of Rs 50/gm was offered for applying online and paying through digital mode. In five years the value incresed from Rs 4889 to Rs 15512/SGB.

Top / Back to Home Page.

Date: June 05 ,2026.

Monetary Policy Statement, 2026-27 Resolution of the Monetary Policy Committee June 3 to 5, 2026

Excerpts:

MPC voted unanimously to keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 5.25 per cent.

Consequently, the standing deposit facility (SDF) rate remains at 5.00 per cent and

the marginal standing facility (MSF) rate and the Bank Rate remain at 5.50 per cent.

The MPC also decided to continue with the neutral stance.

Read More

Latest RBI Policy Rates-Repo Rate, Bank Rate, CRR, SLR etc---

Top / Back to Home Page.

Bank Fixed Deposit Interest Rates-Public and Private Banks

updated on June 03, 2026.

| Banks |

1 Year |

3 years |

5 years |

Max Interest |

| Bank of Baroda |

6.25 |

6.25 |

6.30 |

6.45-444 days |

| Bank of India |

6.50 |

6.25 |

6.00 |

6.85-999 days |

| Canara Bank |

6.25 |

6.25 |

6.25 |

6.60 555days |

| Central Bank |

6.10 |

6.00 |

6.00 |

6.65-333 days |

| Indian Bank |

6.10 |

6.05 |

6.00 |

6.45-444days |

| Indian Overseas Bank |

6.50 |

6.10 |

6.10 |

6.60-444days |

| Punjab National Bank |

6.25 |

6.30 |

6.35 |

6.60-444 days |

*

| Punjab and Sind Bank |

5.85 |

5.85 |

5.95 |

6.75-666 days |

| UCO Bank |

6.10 |

6.00 |

6.00 |

6.60-535 days |

| Union Bank |

6.20 |

6.10 |

6.00 |

6.50-444 days |

*

| State Bank of India |

6.25 |

6.30 |

6.05 |

6.45-444 days |

| IDBI Bank. |

6.20 |

6.35 |

6.25 |

6.45--700 days |

| HDFC Bank |

6.25 |

6.45 |

6.40 |

6.50-3yr+1day |

| ICICI Bank. |

6.25 |

6.45 |

6.50 |

6.50-3yr+1 day |

| Axis Bank |

6.25 |

6.45 |

6.45 |

6.45-15 months |

| SCB Bank. |

6.60 |

6.50 |

6.25 |

6.60-1 year |

| Deposit Interest Rates subject to change . |

| Confirm Interest Rates from respective banks . |

| Please note most of the Banks offer additional 0.50 % interest to Senior Citizens |

| Confirm Interest Rates from respective banks . |

| Top |

Home |

Date: May 30,2026.

Premature redemption under Sovereign Gold Bond (SGB) Scheme - Redemption Price for premature redemption of SGB 2021-22 Series-II

Excerpts:

The due date of premature redemption of the above tranche shall be on June 01, 2026.

The redemption price for premature redemption due on June 01, 2026, shall be ₹15,672/- (Rupees Fifteen Thousand Six Hundred and Seventy Two only) per unit of SGB

Read More.

Note: The issue price of the above SGB was Rs 4,842 per unit of SGB.A further reduction of Rs 50/gm was offered for applying online and paying through digital mode.

In five years the value incresed from Rs 4832 to Rs 15672/SGB.

---------------------------------------------------------------------------

Date: May 30,2026.

Department of Financial Services Launches Common Landing Portal for Unclaimed Financial Assets

Excerpts:

Single unified online platform for citizens to search and trace unclaimed bank deposits, insurance claims, shares and mutual funds across the financial ecosystem

The Portal will improve citizen convenience and strengthen efforts to reconnect individuals with their rightful financial assets.

Read More

Visit the Portal for Unclaimed Financial Assets

ITR-1 (Sahaj) Online User Manual

Read More

Top / Back to Home Page.

Date: May 29,2026.

RBI Press Release- Quantum Secure and Adaptive Financial Ecosystem (Q-SAFE) – Setting up of an Expert Committee

Excerpts:

The Terms of Reference of the Committee are:

Explore and evaluate the potential benefits, risks and challenges in the financial sector.

Evaluate the financial sector's cryptographic inventory through a Cryptography Bill of Materials (CBOM), assess crypto agility and identify the critical systems and processes most vulnerable to such threats.

Undertake a cross-country analysis and assess the adequacy of existing regulatory frameworks for safe deployment of quantum applications.

Evaluate industry preparedness for quantum-safe cryptography adoption, including the availability, scalability, and maturity of vendor tools and solutions.

Recommend a roadmap and framework to quantum-secure the Indian financial system.

Any other areas incidental to the objective.

Read More.

Date: May 29,2026.

India’s Insolvency Framework

Excerpts:

India’s insolvency framework has undergone a major transformation through the Insolvency and Bankruptcy Code, 2016 (IBC).

It introduced a unified, creditor-driven and time-bound mechanism for resolving financial distress. Over the years, the Code has strengthened recovery mechanisms and improved resolution outcomes.

Read More

THE INSOLVENCY AND BANKRUPTCY CODE, 2016

Top / Back to Home Page.

Date: May 23,2026.

Premature redemption under Sovereign Gold Bond (SGB) Scheme -

SGB 2021-22 Series-I

Excerpts:

The due date of premature redemption of the above tranche shall be on May 25, 2026.

The redemption price for premature redemption due on May 25, 2026, shall be ₹15,840/- (Rupees Fifteen Thousand Eight Hundred and Forty only) per unit of SGB

Read More

Note :The issue price of the bond at the time of purchse in May 2021 was just Rs 4777 per unit of SGB.

A discount of Rs 50 per gram was allowed to investors who apply online and the payment is made through digital mode.

The investment value increased more than three times in five years.

Read More

Top / Back to Home Page.

Date:May 17.05.2026.

FAQs on New Tax vs Old Tax Regime

It is time to think of filing Income Tax returns. For salaried Individuals and Pensioners 31st July 2026 is last date for filing the returns for FY 2025-26.

For the benefit of tax payers Income Tax Department posted FAQs on New Tax vs Old Tax Regime in their website.

Follow the link given below to know more.

Excerpts:

What is the difference between the old and new tax regime?

Which is better between the old tax regime and the new tax regime?

Is it necessary for the employee to intimate the tax regime to the employer?

I am a salaried taxpayer. Can I claim HRA exemption in the new regime?

Am I eligible for Rs. 50,000 standard deduction in the new tax regime?

In the new tax regime can I claim deductions under chapter-VIA like section 80C, 80D, 80DD, 80G etc. while filing the ITR for AY 2024-25?

Can I claim deduction of Interest on borrowed capital of Rs. 2,00,000/- for self occupied property under Income from House Property in the new tax regime?

I am a senior citizen. In the old tax regime there are special advantages in tax rates for senior citizens. Are there any such advantages in new tax regime?

Is there any difference in tax rebate under section 87A in old and new tax regime?

Read More.

Top / Back to Home Page.

Date:May 05,2026.

Bank Fixed Deposit Interest Rates-Public and Private Banks

updated on May 05, 2026.

| Banks |

1 Year |

3 years |

5 years |

Max Interest |

| Bank of Baroda |

6.10 |

6.25 |

6.30 |

6.45-444 days |

| Bank of India |

6.25 |

6.25 |

6.00 |

6.60-450 days |

| Canara Bank |

6.25 |

6.25 |

6.25 |

6.50 555days |

| Central Bank |

6.20 |

6.00 |

6.00 |

6.30-444 days |

| Indian Bank |

6.10 |

6.05 |

6.00 |

6.45-444days |

| Indian Overseas Bank |

6.50 |

6.10 |

6.10 |

6.60-444days |

| Punjab National Bank |

6.25 |

6.30 |

6.10 |

6.60-444 days |

| Punjab and Sind Bank |

5.85 |

5.85 |

5.95 |

6.75-666 days |

| UCO Bank |

6.10 |

6.00 |

6.00 |

6.45-444 days |

| Union Bank |

6.25 |

6.20 |

6.00 |

6.60-444 days |

| State Bank of India |

6.25 |

6.30 |

6.05 |

6.45-444 days |

| IDBI Bank. |

6.20 |

6.35 |

6.25 |

6.45-->2yr to <3yr |

| HDFC Bank |

6.25 |

6.45 |

6.40 |

6.50-3yr+1day |

| ICICI Bank. |

6.25 |

6.45 |

6.50 |

6.50-3yr+1 day |

| Axis Bank |

6.25 |

6.45 |

6.45 |

6.45-15 months |

| SCB Bank. |

6.60 |

6.50 |

6.25 |

6.60-1 year |

| Deposit Interest Rates subject to change . |

| Confirm Interest Rates from respective banks . |

| Top |

Home |

Date May 04,2026.

RBI reiterates caution against unauthorised and misleading campaigns promising Loan Waivers

Excerpts:

These campaigns, among others, involve

(i) false promises of waiver of outstanding dues to banks / Non-Banking Financial Companies (NBFCs);

(ii) issuance of ‘debt waiver certificates’ or similar documents; and

(iii) collection of fees under various pretexts, including service or legal charges, from uninformed public. It is reiterated that any claims by individuals / entities offering such services are false, misleading, and liable to attract appropriate legal action under applicable Statutes.

Members of the public are therefore requested to refrain from associating with or availing services from such individuals / entities.

Read More

Top / Back to Home Page.

Date May 02, 2026.

Reserve Bank of India (Commercial Banks – Credit Risk Management) Third Amendment Directions, 2026

Excerpts:

Read More

Reserve Bank of India (Commercial Banks – Resolution of Stressed Assets) Second Amendment Directions, 2026

Excerpts:

Read More

Reserve Bank of India (Commercial Banks – Resolution of Stressed Assets) Directions, 2025

Excerpts:

Read More

Final redemption under Sovereign Gold Bond (SGB) Scheme - Redemption Price for final redemption of SGB 2018-19 Series-I due on May 04, 2026

Excerpts:

The final redemption date of the above tranche shall be May 04, 2026.

The redemption price for final redemption due on May 04, 2026, shall be ₹14901/- (Rupees Fourteen Thousand Nine Hundred and One only) per unit of SGB

Read More

Top / Back to Home Page.

Date April 28,2026.

Reserve Bank of India (Commercial Banks - Capital Charge for Credit Risk – Standardised Approach) Directions, 2026

Read More

RBI issues Directions on Asset Classification, Provisioning, and Income Recognition for Commercial Banks

Read More

Top / Back to Home Page.

Date April 22,2026.

RBI issues Consolidated directions on Digital Payments – E-mandate framework, 2026

Read RBI Notification.

Digital Payments – E-mandate Framework, 2026

Excerpts:

A customer desirous of opting for e-mandate facility shall undertake a one-time registration process. The mandate shall be registered only after successful validation of additional factor of authentication (AFA), in addition to the normal process required by the issuer.

Every e-mandate registered by the issuer shall specify the validity period of the e-mandate.

The e-mandate may be for either a pre-specified fixed amount or for a variable amount subject to the overall cap fixed by the RBI

The first transaction under an e-mandate shall require AFA validation.

Pre-transaction Notification

(a) An issuer shall send a pre-transaction notification to the customer, at least 24 hours prior to the actual charge / debit.

(b) The pre-transaction notification shall, at the minimum, inform the customer about the merchant’s name, transaction amount, date / time of debit, reference number of e-mandate, reason for debit, i.e., e-mandate registered by the customer.

(c) The issuer shall provider a customer with a facility to opt-out of any particular transaction or the e-mandate. Any such opt-out shall be validated by the issuer using AFA. An intimation to this effect shall be sent to the customer.

Read RBI Master Directions

Date April 17,2026.

RBI issues Amendment Directions on ‘Non-Banking Financial Companies – Branch Authorisation Directions’

Read More

Reserve Bank of India (Non-Banking Financial Companies – Branch Authorisation) Amendment Directions, 2026

Read More

Reserve Bank of India (Non-Banking Financial Companies – Acceptance of Public Deposits) Directions, 2025 (Updated as on April 15, 2026)

Read More.

Reserve Bank of India (Housing Finance Companies) Directions, 2025 (Updated as on April 15, 2026)

Read More.

Top / Back to Home Page.

Date April 14,2026.

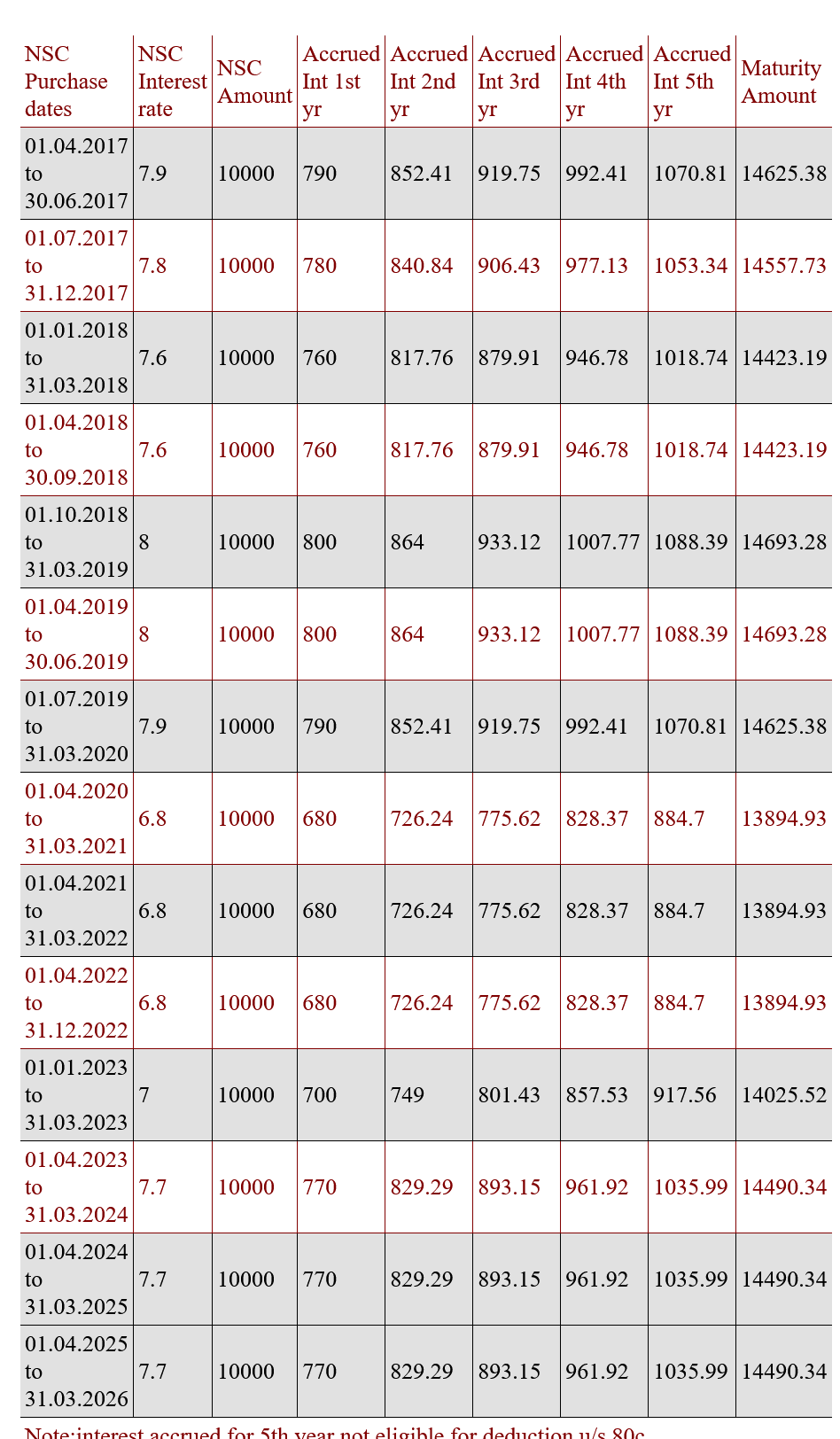

NSC-National Savings Certificae-Interest Rates,Yearly Interest Accretion,Maturity Value Chart- From 2017 to 2026

Read More

Top / Back to Home Page.

Date April ,2026.

RBI invites comments on the Draft “Reserve Bank of India (Branch Authorisation) Amendment Directions, 2026”

Read More

Draft – Reserve Bank of India (Commercial Banks - Branch Authorisation) Amendment Directions, 2026

Read More

Reserve Bank of India (Commercial Banks - Branch Authorisation) Directions, 2025

Read More

Top / Back to Home Page.

Post Office Small Savings Interest Rates-FY 2026-27.

Interest Rates unchanged for the quarter April 2026 to June 2026.

| Scheme Name |

2026

Apr-Jun |

2026

Jul-Sep |

2026

Oct-Dec |

2027

Jan-Mar |

| Savings Deposit |

4.00 |

**** |

**** |

**** |

| 1 Year Time Deposit |

6.90 |

**** |

**** |

**** |

| 2 Year Time Deposit |

7.00 |

**** |

**** |

**** |

| 3 Year Time Deposit |

7.10 |

**** |

**** |

**** |

| 5 Year Time Deposit |

7.50 |

**** |

**** |

**** |

| 5 Year Recurring Deposit |

6.70 |

**** |

**** |

**** |

| 5yr Senior Citizen's Savings |

8.20 |

**** |

**** |

**** |

| 5yr Monthly Income Deposit |

7.40 |

**** |

**** |

**** |

| National Savings Certificate. |

7.70 |

**** |

**** |

**** |

| Public Provident Fund |

7.10 |

**** |

**** |

**** |

| Kisan Vikas Patra |

7.50 |

**** |

**** |

**** |

| Sukanya Samriddhi Account. |

8.20 |

**** |

**** |

**** |

Know your NSC Accrued Interest eligible for deduction from Income tax for FY 2026-27.

Nsc Yearwise-Interest Accretion-Chart

March 21, 2026.

All about income tax on salary-Financial Year 2025-26.

A comprehensive guide.

Income Tax Calculator- FY 2025-26.

Income Tax Rates FY 2025-26.

Finance Bill 2025

Income Tax Act 1961-Asamended by Finance Act 2025

Income Tax important sections for availing deductions from Income.

Deduction limits

NSC VIII th Issue -Interest eligible for deduction U/S 80C FY 2025-26.

NSC Interest and Maturity Value Calculator

NSC Accrued Interest Chart

HRA Rebate Calculator.

***************************************************************

Important points to remember:

Standard Deductions:

Standard Deductions -New Tax Regime Max Rs 75000.

Standard Deductions Old Tax Regime Max Rs 50000.

Standard Deductions Family Pensioners Max Rs 25000.

Section 87A. New Tax Regime

A resident individual (whose net income does not exceed Rs. 7,00,000) can avail rebate under section 87A.

It is deductible from income-tax before calculating education cess.

The amount of rebate is 100 per cent of income-tax or Rs. 25000, whichever is less.

Section 87A: Old Tax Regime

A resident individual (whose net income does not exceed Rs. 5,00,000) can avail rebate under section 87A.

It is deductible from income-tax before calculating education cess.

The amount of rebate is 100 per cent of income-tax or Rs. 12,500, whichever is less.

Section 80TTA-Interest frrom Savings Bank Account: Old Tax Regime

For Individuals other than senior Citizens :Max Rs10000.

Interest on Fixed and other deposits not allowed.

Section 80TTB-Interest frrom Savings Bank and Fixed Deposit Accounts Account: Old Tax Regime

For Senior Citizens :Interest from Savings and Fixed Deposit Accounts:

Max Rs50000.

Thank you for visiting my Website.

Your suggestions / Comments will help me improve this page.

You may E-mail your suggestions/ comments to "ssm_dindigul@yahoo.co.in"

Subramanian S (Retd Manager,United Bank of India.)

-->

Date February 25,2026.

Sovereign Gold Bond (SGB) Scheme

Calendar for premature redemption during April 2026 – September 2026

Read More

Sovereign Gold Bond Scheme of the Government of India (GoI) - Procedural Guidelines - Consolidated (Updated as on October 04, 2022)

Read More

Minutes of the Monetary Policy Committee Meeting, February 4 to 6, 2026

Excerpts:

The MPC voted unanimously to keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 5.25 per cent.

Consequently, the standing deposit facility (SDF) rate remains at 5.00 per cent and

The marginal standing facility (MSF) rate and the Bank Rate remains at 5.50 per cent.

The MPC also decided to continue with the neutral stance.

Read More.

Top / Back to Home Page.

Date February 13,2026.

RBI Issues Draft Amendment Directions for ‘Conduct of Regulated Entities in Recovery of Loans and Engagement of Recovery Agents’

Excerpts:

Detailed instructions on matters related to engagement of recovery agents have been issued to Scheduled Commercial Banks (excluding Regional Rural Banks) and Housing Finance Companies currently.

Upon a review, it has been decided to issue comprehensive instructions to all regulated entities on conduct related matters in recovery of loans and engagement of recovery agents, which inter alia cover aspects such as fair treatment to borrowers during recovery process, conduct of lender’s employees and recovery agents, due diligence, training, code of conduct for recovery agents, etc.

(RBI) has today issued the following draft Amendment Directions for public comments, which propose to amend existing Directions issued by the Department of Regulation, RBI.

Reserve Bank of India (Commercial Banks - Responsible Business Conduct) Second Amendment Directions, 2026

Reserve Bank of India (Small Finance Banks - Responsible Business Conduct) Second Amendment Directions, 2026

Reserve Bank of India (Local Area Banks - Responsible Business Conduct) Second Amendment Directions, 2026

Reserve Bank of India (Regional Rural Banks - Responsible Business Conduct) Second Amendment Directions, 2026

Reserve Bank of India (Urban Co-operative Banks - Responsible Business Conduct) Second Amendment Directions, 2026

Reserve Bank of India (Rural Co-operative Banks - Responsible Business Conduct) Second Amendment Directions, 2026

Reserve Bank of India (All India Financial Institutions - Responsible Business Conduct) Second Amendment Directions, 2026

Reserve Bank of India (Non-Banking Financial Companies - Responsible Business Conduct) Second Amendment Directions, 2026

Reserve Bank of India (Housing Finance Companies) Second Amendment Directions, 2026

Read More

Top / Back to Home Page.

Date February 12,2026.

Revised Kisan Credit Card (KCC) Scheme

Excerpts:

The following major changes in the KCC Scheme are reflected in the draft guidelines:

To bring in uniformity in loan sanction and repayment schedules, crop seasons have been standardized in terms of months i.e. short duration crops (12 months) and long duration crops (18 months)

To ensure proper dovetailing of loan tenure with crop seasons especially for the longer duration crops, the tenure of KCC has been extended to 6 years.

To ensure that farmers receive adequate credit based on actual cost of cultivation, drawing limits under KCC has been aligned with the scale of finance for each crop season.

To enable farmers to access finance for technological interventions such as soil testing, real time weather forecasts and organic/good agricultural practices certification etc such expenses has been added as eligible components within 20% additional component towards repairs and maintenance of farm assets.

Read More

Top / Back to Home Page.

Date January 18,2026.

Foreign Exchange Management (Export and Import of Goods and Services) Regulations, 2026 and Directions on Export and Import of Goods and Services

Read More

RBI Notification No. FEMA 23(R)/2026-RBI January 13, 2026

Read More

Top / Back to Home Page.

Date January 16,2026.

RBI issues Reserve Bank of India (Internal Ombudsman) Directions, 2026

Read More

Reserve Bank of India (Commercial Banks - Internal Ombudsman) Directions, 2026

Read More

Top / Back to Home Page.

Date January 15,2026.

Reserve Bank of India (Payments Banks - Internal Ombudsman) Directions, 2026

Excerpts:

These Directions are issued with a view to strengthen the Internal Grievance Redress mechanism within a bank and ensure a speedy and meaningful resolution of customer complaints by enabling a review before their rejection, by an apex level authority within the bank.

1. Short Title and Commencement

- (1) These Directions shall be called the Reserve Bank of India (Payments Banks - Internal Ombudsman) Directions, 2026.

- (2) These Directions shall come into force with immediate effect except clause 7(2), 14(2) and 14(4) which shall be complied with, latest by June 30, 2026.

These Directions shall be applicable to Payments Banks (hereinafter collectively referred to as 'banks' and individually as a 'bank') having 10 or more banking outlets in India as on March 31, 2025.

Read More

Read More

Top / Back to Home Page.

Date January 11,2026.

Banking Laws (Amendment) Act, 2025 -Key Points

Excerpts:

- Depositors can nominate up to four persons for their bank accounts via either simultaneous for successive nominations

- Simultaneous nominations allow percentage-wise allocation totalling to 100%

- Successive nominations ensure seamless succession in case of a nominee’s death for articles in safe custody and safety lockers

- Depositors to get flexibility to designate nominees in accordance with their preferences for deposits and lockers.

- Strengthened governance standards and improved audit quality in public sector banks

- Unclaimed funds to be transferred to the Investor Education and Protection Fund

- Updated regulatory norms with modern thresholds and repor ng standards for greater transparency.

The Banking Laws (Amendment) Act, 2025 is a step towards strengthening governance standards in the banking sector by ensuring uniformity in reporting by banks to the Reserve Bank of India along with improved audit quality in public sector banks (PSBs). The act enhances depositor and investor protec on by promoting customer convenience through improved nomina on facili es.

Read More

Banking Laws (Amendment) Act, 2025

Top / Back to Home Page.

Date:November ,2025.

Government Makes the Four Labour Codes effective to Simplify and Streamline Labour Laws

Excerpts: Four Labour Codes Herald Transformational Change: Better Wages, Safety, Social Security & Enhanced Welfare for India’s Workforce

Codes lay the foundation for a protected, future-ready workforce and resilient industries, boosting employment and driving labour reforms for Aatmanirbhar Bharat

Code aligns India’s labour ecosystem with global standards, ensuring social justice for all workers

Read More

Code on Wages, 2019 Safeguards Workers, Induces Growth, Empowers Women & Enhances Employment

Posted On: 23 NOV 2025 11:32AM by PIB Delhi

Read More

Top / Back to Home Page.

Date:Novenber 23,2025.

Interlinking of Unified Payments Interface (UPI) with the TARGET Instant Payment Settlement (TIPS) of the Eurosystem

Excerpts:

Reserve Bank of India has been actively pursuing interlinking of Unified Payments Interface (UPI) with fast payment systems of other jurisdictions to promote cross-border payments.

Reserve Bank of India and NPCI International Payments Limited (NIPL) have been engaging with European Central Bank on the initiative to connect UPI with the TARGET Instant Payment Settlement (TIPS), the instant payment system operated by the Eurosystem.

The proposed UPI–TIPS interlinkage aims to facilitate cross-border remittances between India and the Euro Area and is expected to benefit users of both jurisdictions.

Read More

Top / Back to Home Page.

-->

Date:Novenber 14,2025.

Reserve Bank of India (Nomination Facility in Deposit Accounts, Safe Deposit Lockers and Articles kept in Safe Custody with the Banks) Directions, 2025

Excerpts:

At the time of account opening, a bank shall explicitly inform the prospective customer of the availability and purpose of the nomination facility and offer him/her the option to avail the same.

If the prospective customer chooses not to avail the nomination facility despite being fully informed, the bank shall proceed to open the deposit account without imposing any restrictions, if otherwise found eligible, after obtaining a written declaration from the individual confirming that he/ she does not require the nomination facility at the time of account opening. If he/she refuses to provide the written declaration, the bank shall record the fact of refusal to submit written confirmation in the account opening records.

Under no circumstances shall a prospective customer be denied or delayed in opening an account solely on the ground of refusal to make a nomination, provided all other requirements for account opening are satisfactorily met.

A bank shall record the status regarding registration of nomination on the face of the passbook/ Statement of Account and TDR, with the legend "Nomination Registered".

A bank shall also indicate the name of the Nominee(s) in the Passbook/ Statement of Accounts and TDR in such cases.

Read More

R B I (Settlement of Claims in respect of Deceased Customers of Banks) Directions, 2025

Top / Back to Home Page.

Date:October 25,2025.

Key Provisions relating to Nomination under the Banking Laws (Amendment) Act, 2025 to come into effect from 1st November 2025

Excerpts: The key features of these provisions are as follows:

Multiple Nominations: Customers may nominate up to four persons, either simultaneously or successively, thereby simplifying claim settlement for depositors and their nominees.

Nomination for Deposit Accounts: Depositors may opt for either simultaneous or successive nominations, as per their preference.

Nomination for Articles in Safe Custody and Safety Lockers: For such facilities, only successive nominations are permitted.

Simultaneous Nomination:Depositors may nominate up to four persons and specify the share or percentage of entitlement for each nominee, ensuring that the total equals 100 percent and enabling transparent distribution amongst all nominees.

Successive Nomination: Individuals maintaining deposits, articles in safe custody, or lockers may specify up to four nominees, where the next nominee becomes operative only upon the death of the nominee placed higher, ensuring continuity in settlement and clarity of succession.

The implementation of these provisions will give depositors the flexibility to make nominations as per their preference, while ensuring uniformity, transparency, and efficiency in claim settlement across the banking system.

Read More

THE BANKING LAWS (AMENDMENT) ACT, 2025 No. 16 of 2025.

Top / Back to Home Page.

Date:October 14,2025.

Government Launches Employees' Enrolment Scheme 2025 to Expand Social Security Coverage of Employees

Posted On: 13 OCT 2025 by PIB Delhi

Excerpts:

Scheme to be Operational from November 1, 2025, to April 30, 2026

Scheme to Boost Employee Enrolment under Social Security and help Employers Regularize Past Records

This scheme is intended to encourage employers, both already registered and those newly coming under the purview of the Employees' Provident Funds and Miscellaneous Provisions Act, 1952, to voluntarily declare and enroll eligible employees.

Employers can enroll all existing employees who joined the establishment between July 1, 2017, and October 31, 2025, and who are alive and employed on the date of the declaration, but were not enrolled in the EPF scheme earlier for any reason whatsoever.

The employee's share of provident fund contribution for the past period (from July 1, 2017, to October 31, 2025) shall stand waived, provided it was not deducted from the employee's wages. The employer is only required to pay their own share for such period.

All the employers who get registered under the EES,2025, or declare additional employees under the EES, 2025 shall be eligible to avail the benefits of Pradhan Mantri-Viksit Bharat Rojgar Yojana, subject to certain terms and conditions under that scheme.

Read More

Top / Back to Home Page.

Date:October 14,2025.

Reserve Bank - Integrated Ombudsman Scheme, 2021 (RB-IOS, 2021) NOTIFICATION

Excerpts from RBI Circular:

The State Co-operative Banks, and Central Co-operative Banks, as defined in the Banking Regulation Act, 1949, shall also be treated as a ‘Regulated Entity’ for the purpose of Reserve Bank - Integrated Ombudsman Scheme, 2021 (the Scheme).

This Notification shall come into force with effect from November 01, 2025.

4. With this inclusion, the Scheme covers the following regulated entities:

All Commercial Banks, Regional Rural Banks, State Co-operative Banks, Central Co-operative Banks, Scheduled Primary (Urban) Co-operative Banks, and Non-Scheduled Primary (Urban) Co-operative Banks with deposits size of ₹50 crore and above as on the date of the audited balance sheet of the previous financial year;

All Non-Banking Financial Companies (excluding Housing Finance Companies) which (a) are authorised to accept deposits; or (b) have customer interface, with an assets size of ₹100 crore and above as on the date of the audited balance sheet of the previous financial year;

All System Participants as defined under the Scheme; and

Credit Information Companies.

Read More

Top / Back to Home Page.

Date:October 10,2025.

Consolidation of Regulations – Drafts for comments

Excerpts:

The existing universe of regulatory instructions issued up to October 9, 2025 have been consolidated into 238 Master Directions, across 11 types of regulated entities on up to 30 functions / areas. Consequently, approximately 9000 circulars (including Master Circulars / Master Directions) administered by the Department of Regulation will be repealed.

the Reserve Bank has placed on its website the following sets of draft documents for comments regarding completeness and accuracy:

Drafts of the 238 consolidated Master Directions / Guidelines.

List of the circulars proposed to be repealed

Read More

Top / Back to Home Page.

Date:October 3,2025.

Draft External Commercial Borrowing Framework under Foreign Exchange Management (Borrowing and Lending) Regulations, 2018

Excerpts:

Salient features of the proposed regulations are as under:

- The borrowing limits are proposed to be linked to a borrower’s financial strength and ECB are proposed to be raised at market determined interest rates.

- The end-use restrictions and Minimum Average Maturity requirements are proposed to be simplified.

- The borrower and lender base eligible for ECB transactions is proposed to be expanded to enhance opportunities of credit flow.

- Reporting requirements are being simplified to ease compliance obligations.

Read More

Draft Foreign Exchange Management (Establishment in India of a branch or office) Regulations, 2025

Excerpts: It has been decided to amend the extant regulations along the following lines:

- The eligibility criteria for establishment of a place of business in India, are proposed to be relaxed.

- The draft proposals offer greater operational freedom by shifting from prescriptive to a principle-based framework, which is expected to result in greater operational freedom.

- The process for closure of non-compliant and inactive branch/office, are proposed to be simplified.

Read More. Top / Back to Home Page.

Date:October 02,2025.

RBI Issues draft Directions/ Circulars Excerpts:

In pursuance of the announcement made in the Statement on Developmental and Regulatory Policies dated October 1, 2025, the Reserve Bank of India (RBI) has today issued the following draft Directions/ Circulars for public comments:

- 1. Reserve Bank of India (Transaction Accounts) Directions, 2025

- i.Reserve Bank of India (Commercial Banks – Transaction Accounts) Directions, 2025

- ii.Reserve Bank of India (Small Finance Banks – Transaction Accounts) Directions, 2025

- iii.Reserve Bank of India (Regional Rural Banks – Transaction Accounts) Directions, 2025

- iv.Reserve Bank of India (Local Area Banks – Transaction Accounts) Directions, 2025

- v.Reserve Bank of India (Urban Co-operative Banks – Transaction Accounts) Directions, 2025

- vi.Reserve Bank of India (Rural Co-operative Banks – Transaction Accounts) Directions, 2025

- vii.Reserve Bank of India (Payments Banks – Transaction Accounts) Directions, 2025

- 2. Guidelines on Enhancing Credit Supply for Large Borrowers through Market (Repeal Circular), 2025

- 3. Reserve Bank of India (Basic Savings Bank Deposit Account) Directions, 2025

- Read More

Top / Back to Home Page.

Date:September 27,2025.

Reserve Bank of India (Settlement of Claims in respect of Deceased Customers of Banks) Directions, 2025

Excerpts:

A deposit account where a depositor had made nomination in terms of the provisions of the Banking Regulation Act, 1949 or where the account was opened with survivorship clause, the payment of the outstanding balance upon the death of the depositor(s) to the nominee(s)/ survivor(s) shall be considered a valid discharge of a bank’s liability, provided:

- (i) the bank has exercised due care and caution in establishing the identity of the nominee(s)/ survivor(s) and the deceased status of the account holder(s) by obtaining appropriate documentary evidence (physical or equivalent e-document);

- (ii) there is no order from the competent court in the knowledge of the bank, as on the date of settlement/ payment, restraining the nominee(s)/ survivor(s) from receiving or the bank from making the payment from the account of the deceased depositor(s); and

- (iii) it has been made clear in writing to the nominee(s)/ survivor(s) that they would be receiving the payment from the bank as a trustee of the legal heirs of the deceased depositor(s), i.e., such payment to them shall not affect the right or claim which any person may have against the nominee(s)/ survivor(s) to the extent of the payment made to them.

- In the case of a joint deposit account with or without survivorship clause, the nominee's right arises only after the death of all the depositors.

Payment made to the nominee(s)/ survivor(s), subject to the foregoing conditions, shall constitute a full and valid discharge of a bank's liability.

Therefore, in such cases, while making payment to the nominee(s)/ survivor(s) of the deceased depositor(s), the bank shall not insist on production of legal documents such as Succession Certificate, Letter of Administration, Probate of Will, etc., or seek any bond of indemnity/ surety from the nominee(s)/ survivor(s)/ third-party, irrespective of the amount standing to the credit of the deceased account holder(s).

The bank shall require submission of the following documents in such cases:

- Claim form, as given in Annex I-A, duly signed by the nominee(s)/ survivor(s);

- Death certificate of the deceased depositor(s); and

- Officially Valid Document of the nominee/ survivor towards verifying her/ his identity and address.

Accounts without nominee/ survivorship clause

Simplified Procedure for settlement of claims Keeping in view the imperative need to avoid inconvenience and undue hardship to the legal heir(s)/ claimant(s), a bank shall follow a simplified procedure for settlement of claims in respect of deposit accounts where the aggregate amount payable, including accrued interest, as on the date of the application is less than the threshold limit, provided

- (i) a deceased depositor(s) had not made any nomination or in case of a joint account, the account was without nominee/ survivorship clause,

- (ii) there is no Will left behind by the deceased depositor(s),

- (iii) there is no contesting claim, and

- (iv) there is no order from a competent court in the knowledge of the bank, restraining the claimant(s) from receiving nor the bank from making the payment.

(a) Claim amount up to the threshold limit

The bank shall settle the claim up to the threshold limit based on

- Claim form, as given in Annex I-B, duly filled in and signed by the claimant(s) other than those who have signed the letter of disclaimer/ no objection;

- Death certificate of the deceased depositor(s);

- Officially Valid Document of the claimant(s) towards verifying his/ her identity and address;

- Bond of indemnity, as given in Annex I-C, signed by the claimant(s);

- Letter of disclaimer/ no objection, as given in Annex I-D, from non-claimant legal heir(s), if applicable; and

- Legal Heir Certificate issued by a competent authority;

- OR Declaration, as given in Annex I-E, regarding the legal heir(s) of the deceased depositor(s) by an independent person who is well known to the family of the deceased, is not a party to the claim and is acceptable to the bank.

No bond of surety from a third-party shall be obtained in case of claims up to the threshold limit. (b) Claim amount above the threshold limit In cases where claim amount is above the threshold limit, the bank shall settle the claim based on

- (i) Succession Certificate and documents mentioned at clauses 10(a)(i) to (iii) above; OR

- (ii) Legal Heir Certificate issued by a competent authority; or

- Affidavit, as given in Annex I-E, sworn before a Notary Public/ Judge/ Judicial Magistrate regarding the legal heir(s) of the deceased depositor, by an independent person who is well known to the family of the deceased, is not a party to the claim and is acceptable to the bank.

- In such cases, the bank shall call for the documents at clauses 10(a)(i) to (v) above. The bank may also call for a bond of surety, as given in Annex I-C, from third-party individuals (which may include non-claimant legal heir(s)) who are acceptable to the bank and good for the claim amount.

Read More

Read RBI Circular

Top / Back to Home Page.

Date:September 26,2025.

RBI-authentication-mechanisms-for-digital-payments.pdf

Excerpts: Effective Date:April 01, 2026,unless indicated otherwise for any specific provision herein.

Definitions: I. Unless the context otherwise requires, the following terms shall bear the meanings assigned to them as below:

Authentication: Process of validating and confirming the credentials of the customer who is originating the payment instruction.

Factor of Authentication: Credential of the customer which is used for authentication. The factors of authentication can be from “something the user has”, “something the user knows” or “something the user is” and may comprise, inter-alia, password, SMS based OTP, passphrase, PIN, card hardware, software token, fingerprint, or any other form of biometrics (device native or Aadhaar based).

6. Principles for authentication of digital payment transactions

a. Minimum two factors of authentication All digital payment transactions shall be authenticated by at least two distinct factors of authentication as defined in paragraph-5(f), unless exempted. The list of exemptions which are currently in force are listed in Annexure-1.

Note - Issuers may, at their discretion, offer a choice of authentication factors to their customers in compliance with these directions.

b. At least one of the factors to be dynamic

It shall be ensured that for digital payment transactions, other than card present transactions, at least one of the factors of authentication is dynamically created or proven, i.e., the proof of possession of the factor, being sent as part of the transaction, is unique to that transaction.

c. Robust The factor of authentication shall be such that compromise of one factor does not affect reliability of the other.

Responsibility of the issuer

An issuer shall ensure the robustness and integrity of the authentication mechanism before deployment.

If any loss arises out of transactions effected without complying with these directions, the issuer shall compensate the customer for the loss in full without demur.

Issuers shall ensure adherence to the provisions of Digital Personal Data Protection Act, 2023.

Read RBI Circular.

Read More

Top / Back to Home Page.

Date:September 22,2025.

The Income Tax Act, 2025 Reshaping Tax Framework-PIB Posted On: 03 SEP 2025

Excerpts: Income Tax Act, 2025 to be effective from April 1, 2026.

The Act simplifies language, removes obsolete provisions and consolidates and restructures provisions.

It Introduces concept of ‘Tax Year’ replacing ‘Assessment Year’ and ‘Previous Year’.

The Act defines Virtual Digital Assets (VDAs), including cryptocurrencies and tokenized assets.

Read More

Read more"Income Tax Act 2025".

INCOME TAX DAY, 2025-A journey of Digital Transformation July 23, 2025

Read More.

INCOME-TAX ACT, 1961*[43 OF 1961]

[AS AMENDED BY FINANCE ACT, 2025]

Read More

Top / Back to Home Page.

Date:September17,2025.

Exposure Draft - Amendments to Pension Fund Regulatory and Development Authority (Exits and Withdrawals under the National Pension System) Regulations, 2015

Read More

Unified Pension Scheme

Read more

NPS for All Citizen Model

Read more

Top / Back to Home Page.

Date:September 16,2025.

RBI issues the "Reserve Bank of India (Regulation of Payment Aggregators) Directions, 2025"

Excerpts: The Directions entail, inter-alia, the following:

- Rationalisation of the definition of various categories of PAs;

- The authorisation process;

- The process for carrying out due diligence of merchants by PAs;

- Permissible operations in escrow accounts;

Read More

Master Direction on Regulation of Payment Aggregator (PA)

Read More

Top / Back to Home Page.

Date:August 13,2025.

RBI guidelines ensure multilingual customer communication and a quicker grievance redressal by banks

Excerpts:

Reserve Bank of India (RBI) has, from time to time, emphasised that all customer-facing materials at the branches of Scheduled Commercial Banks must be made available in Hindi, English, and the concerned regional language.

Further, RBI reiterated that all communications to customers, should invariably be issued in a trilingual format-Hindi, English, and the regional language.

All Banks have a robust board approved grievance redressal mechanism in place to address complaints.

Further, the Reserve Bank – Integrated Ombudsman Scheme (RB-IOS), 2021, provides a cost-free platform for redressal of complaints against RBI-regulated entities (REs) in matters relating to deficiency in service,

if the grievance is not redressed or reply is not given by the RE within the prescribed timeline.

Read More

Top / Back to Home Page.

Date:August 08 ,2025.

RBI invites comments on Settlement of claims in respect of deceased depositors – Simplification of Procedure

Excerpts:

In pursuance of the announcement made in the Statement on Developmental and Regulatory Policies dated August 06, 2025 regarding the review of extant regulatory guidelines on settlement of claims in respect of deceased depositors, Reserve Bank has released today the draft circular in this regard.

Comments/ feedback by the stakeholders and members of public on the draft circular may be submitted through the respective link under the ‘Connect 2 Regulate’ Section available on the Reserve Bank’s website or alternatively through e-mail by August 27, 2025. Final circular shall be issued after considering the stakeholder/ public comments.

Read More

settlement-of-claims-in-respect-of-deceased-customers-rbi-draft-circular.pdf

Settlement of claims in respect of deceased depositors – Simplification of procedure.pdf

Top Back to Home Page.

Date:August 02,2025.

Income Tax-Deductions allowed from Income-FY 2025-26

Excerpts:

Against 'salaries'

Standard Deduction

(a) In case of normal tax regime - Rs. 50,000 or the amount of salary, whichever is lower;

(b) In case of new tax regime under section 115BAC(1A)(ii) - Up to Rs. 75,000 or the amount of salary, whichever is lower

Individual – Salaried Employee & Pensioners

Against 'income from house properties'

23(1), first proviso Taxes levied by local authority and borne by owner if paid in relevant previous year All assessees

24(a) Standard deduction [30% of the annual value (gross annual value less municipal taxes)] All assessees

24(b) Interest on borrowed capital (Rs. 30,000/Rs. 2,00,000, subject to specified conditions) All assessees

25A(2) Standard deduction of 30 per cent of arrears of rent or unrealised rent received All assessees

Against 'income from other sources'

A. Deductible items

57(i) Deduction from dividend income on account of interest expense, which shall not exceed 20% of the dividend income. All assessees

57(i) Any reasonable sum paid by way of commission or remuneration for the purpose of realising interest on securities All assessees

57(ia) Contributions to any provident fund or superannuation fund or any fund set up under Employees' State Insurance Act, 1948 or any other fund for welfare of employees, if the same are credited to employees' accounts in relevant funds before due date All assessees

57(ii) Repairs, insurance, and depreciation of building, plant and machinery and furniture Assessees engaged in business of letting out of machinery, plant and furniture and buildings on hire

57(iia)

In case of family pension, 331/3 per cent of such pension or Rs. 15,000, whichever is less

Note: the enhanced threshold of Rs. 25,000 shall be applicable if income-tax is computed under section 115BAC(1A)(ii).

Assessees in receipt of family pension on death of employee being member of assessee's family

57(iii) Any other expenditure (not being capital expenditure) expended wholly and exclusively for earning such income All assessees

57(iv) In case of interest received on compensation or on enhanced compensation referred to in section 145A(2), a deduction of 50 per cent of such income (subject to certain conditions)

Read Income Tax Department Circular

Some Important Sections

Note:Only some selected sections are given and for personal use only. Most of the deductions are not allowed under New Tax Regime. All Rules ,Regulations ,Eligibility and Limits are subject to change. Before taking any decisions check up relevant rules or seek advice from tax consultant.

Top / Back to Home Page.

Date:July 10,2025.

Reserve Bank of India (Pre-payment Charges on Loans) Directions, 2025

Excerpts:

Regulated Entities (REs) shall adhere to the following Directions regarding levy of pre-payment charges on all floating rate loans and advances:

(i) For all loans granted for purposes other than business to individuals, with or without co-obligant(s), an RE shall not levy pre-payment charges;

(ii) For all loans granted for business purpose to individuals and MSEs, with or without co-obligant(s):

(a) A commercial bank (excluding Small Finance bank, Regional Rural bank and Local Area bank), a Tier 4 Primary (Urban) Co-operative bank, an NBFC-UL, and an All India Financial Institution shall not levy any pre-payment charges.

(b) A Small Finance bank, a Regional Rural bank, a Tier 3 Primary (Urban) Co-operative bank, State Cooperative bank, Central Cooperative bank and an NBFC-ML shall not levy any pre-payment charges on loans with sanctioned amount/ limit up to ₹50 lakh.

(iii) The Directions at paragraphs 5(i) and 5(ii) above shall be applicable irrespective of the source of funds used for pre-payment of loans, either in part or in full, and without any minimum lock-in period.

(iv) Applicability of above Directions for dual/ special rate (combination of fixed and floating rate) loans will depend on whether the loan is on floating rate at the time of pre-payment.

6. In cases other than those mentioned at paragraphs 5(i) and 5(ii) above, pre-payment charges, if any, shall be as per the approved policy of the RE. However, in case of term loans, pre-payment charges, if levied by the RE, shall be based on the amount being prepaid. In case of cash credit/ overdraft facilities, pre-payment charges on closure of the facility before the due date shall be levied on an amount not exceeding the sanctioned limit.

7. In case of cash credit/ overdraft facilities, no pre-payment charges shall be applicable if the borrower intimates the RE of his/ her/ its intention not to renew the facility before the period as stipulated in the loan agreement, provided that the facility gets closed on the due date.

8. An RE shall not levy any charges where pre-payment is effected at the instance of the RE.

Read More

Top / Back to Home Page.

Date:June 29,2025.

Aadhaar Enabled Payment System – Due Diligence of AePS Touchpoint Operators

Excerpts:

Aadhaar Enabled Payment System (AePS) is a payment system operated by National Payment Corporation of India (NPCI) that facilitates interoperable transactions using Aadhaar enabled authentication. AePS plays a prominent role in enabling financial inclusion.

It has been decided to issue directions for streamlining the process for onboarding of AePS touchpoint operators and strengthening fraud risk management. Detailed instructions are placed in the Annex.

Read More

Top / Back to Home Page.

Date:June 13,2025.

Updation/ Periodic Updation of KYC – Revised Instructions-RBI Notfication dated June 12,2025

Excerpts:

The Reserve Bank has observed a large pendency in periodic updation of KYC including in the accounts opened for credit of Direct Benefit Transfer (DBT)/ Electronic Benefit Transfer (EBT) under Government schemes to facilitate credit of DBTs and/ or scholarship amount (DBT/ EBT/ scholarship beneficiaries) and accounts opened under PMJDY.

The instructions regarding updation/ periodic updation of KYC have been amended with the intent, inter alia, to allow BCs to facilitate in the process of KYC updation

The banks are advised to organize camps and launch intensive campaigns including special camps, focusing on periodic updation of KYC

Read more

Inoperative Accounts/ Unclaimed Deposits in Banks - Revised Instructions (Amendment) 2025

Excerpts:

The credit balance in any deposit account maintained with banks, which have not been operated upon for ten years or more, or any amount remaining unclaimed for ten years or more are required to be transferred by banks to DEA Fund maintained by the Reserve Bank of India. There is a need to enable Business Correspondents to facilitate updation of KYC.

In the extant instructions, the paragraph 6.1 is hereby substituted by the following, namely:

“6.1 A bank shall make available the facility of updation of KYC for activation of inoperative accounts and unclaimed deposits at all branches (including non-home branches).

Further, a bank shall endeavour to provide the facility of updation of KYC in such accounts and deposits through Video-Customer Identification Process (V-CIP).

The V-CIP related instructions under Master Direction - Know Your Customer (KYC) Direction, 2016 dated February 25, 2016 (as updated from time to time) shall be adhered to by the bank.

Additionally, the services of an authorised Business Correspondent of the bank may be utilized for activation of inoperative accounts as prescribed in paragraph 38(a)(iia) of the above Master Direction.”.

Read More

Top / Back to Home Page.

12Th Bipartite Settlement.

11Th Bipartite Settlement.

Joint Note 9-Bank officers' settlement

Joint Note 8-Bank officers' settlement

Gratuity Act 1972.

Gratuity Amendment 2018.

Brief on Gratuity Amendment 2018

Banking Regulations Act 1949.

Bankers Book Evidence Act 1891

Payment of Wages Act 1936

prevention of Money Laundering Act 2002.

Pensions Act.

Income Tax Bill 2025.

Finance Bill 2025.

Income Tax Act 1961

As amended-by-finance-no.-2-act-2024

Top / Back to Home Page.

Date:May 10,2025.

RBI issues Reserve Bank of India (Digital Lending) Directions, 2025

Excerpts:

Consolidated directions on the subject have been prepared and issued as the Reserve Bank of India (Digital Lending) Directions, 2025 today.

A draft circular on the aforesaid matter was issued on April 26, 2024, for public feedback. Basis the comments received, final instructions on the same are being issued as part of these Directions.

The instructions require REs to furnish the details of their DLAs through the Centralised Information Management System (CIMS) portal of the RBI. The portal shall be available to the REs for reporting on or before May 13, 2025 and REs shall have time till June 15, 2025 to upload the initial data.

RBI press release.

Reserve Bank of India (Digital Lending) Directions, 2025

Top / Back to Home Page.

04.05.2025.

Post Office Small Savings Schemes-

Scheme details,how to open,minimum amount for opening,interest rates etc

- PO Savings Account(SB)

- PO Recurring Deposit Account(RD)

- PO Time Deposit Account(TD)

- PO Monthly Income Account(MIS)

- PO Senior Citizens Savings Scheme Account(SCSS)

- PO Public Provident Fund Account(PPF )

- PO Sukanya Samriddhi Account(SSA)

- PO Savings Certificates (VIIIth Issue) (NSC)

- PO Kisan Vikas Patra(KVP)

- PO Mahila Samman Savings Certificate

- PM CARES for Children Scheme, 2021

Read more.

Top / Back to Home Page.

Date:24.04.2025.

Migration to '.bank.in' domain-RBI Circular.

Excerpts:

Date:April 18,2025.

RBI issues draft Directions on the regulatory measures announced in SDRP

Excerpts:

Reserve Bank has released the draft Directions on the following subjects for comments.

Draft Reserve Bank of India (Securitisation of Stressed Assets) Directions, 2025

Draft Reserve Bank of India (Co-Lending Arrangements) Directions, 2025

Draft Reserve Bank of India (Lending Against Gold Collateral) Directions, 2025

Draft Reserve Bank of India (Non-Fund Based Credit Facilities) Directions, 2025

The comments on the draft Directions are invited from public/stakeholders till May 12, 2025. Comments/feedback may be submitted through the respective links under the ‘Connect 2 Regulate’ Section available on the RBI’s website or may alternatively be forwarded to:

The Chief General Manager

Credit Risk Group

Department of Regulation, Central Office

Reserve Bank of India, 12/13th Floor,

Shahid Bhagat Singh Marg,

Fort Mumbai – 400 001 Or by email

RBI Press Release: 2025-2026/69

Top/Home

Date:April 17,2025.

Master Direction - Deposits and Accounts

Foreign Currency and other Accounts

read more.

Master Direction - Risk Management and Inter-Bank Dealings

read more

Date:April 10,2025.

Effect of Repo rate on loan EMI-what is your gain or loss due to change in repo rate.

RBI reduced Repo rate by 25 basis points.The revised Repo Rate is 6.00 %. Normally Banks are expected to change their interest rates on loans. Already some of the banks have reduced the interest rates on loans. Check up with your banks the revised interest rates.Here is a simple calculator to know your Revised EMI , total interest you have to pay during the loan period.

Click for the Calculator.

Know more about Repo Rate ,Bank Rate ,CLR,SRR etc

Date: April 04,2025.

Master Circular - Guarantees and Co-acceptances

Excerpts:

As regards the purpose of the guarantee, as a general rule, the banks should confine themselves to the provision of financial guarantees and exercise due caution with regard to performance guarantee business.

2.1.2 As regards maturity, as a rule, banks should guarantee shorter maturities and leave longer maturities to be guaranteed by other institutions.

2.1.3 No bank guarantee should normally have a maturity of more than 10 years. However, where banks extend long term loans for periods longer than 10 years for various projects, it has been decided to allow banks to also issue guarantees for periods beyond 10 years. While issuing such guarantees, banks are advised to take into account the impact of very long duration guarantees on their Asset Liability Management. Further, banks may evolve a policy on issuance of guarantees beyond 10 years as considered appropriate with the approval of their Board of Directors.

2.1.4 Banks should, in general, refrain from issuing non-fund based facilities to/on behalf of constituents who do not enjoy credit facilities with them. However, banks are permitted to grant non-fund based facilities, including partial credit enhancement1, to those customers, who do not avail any fund based facility from any bank in India.

BG /LC may be issued by scheduled commercial banks to clients of co-operative banks against counter guarantee of the co-operative bank as permitted hitherto.

Precautions for issuing guarantees

Banks should adopt the following precautions while issuing guarantees on behalf of their customers.

- (i) As a rule, banks should avoid giving unsecured guarantees in large amounts and for medium and long-term periods. They should avoid undue concentration of such unsecured guarantee commitments to particular groups of customers and/or trades.

- (ii) Unsecured guarantees on account of any individual constituent should be limited to a reasonable proportion of the bank’s total unsecured guarantees. Guarantees on behalf of an individual should also bear a reasonable proportion to the constituent’s equity.

- (iii) In exceptional cases, banks may give deferred payment guarantees on an unsecured basis for modest amounts to first class customers who have entered into deferred payment arrangements in consonance with Government policy.

- (iv) Guarantees executed on behalf of any individual constituent, or a group of constituents, should be subject to the prescribed exposure norms.

- (v) It is essential to realise that guarantees contain inherent risks and that it would not be in the bank’s interest or in the public interest, generally, to encourage parties to over-extend their commitments and embark upon enterprises solely relying on the easy availability of guarantee facilities.

Read RBI Circular.

Home/Top

Date: April 04,2025.

Master Circular - Disbursement of Government Pension by Agency Banks

Excerpts:

4. The pension paying banks will credit the pension amount in the accounts of the pensioners based on the instructions given by respective Pension Paying Authorities. Refund of excess pension payment to Government

5. Whenever any excess/overpayment is detected, the entire amount thereof should be credited to the Government account in lump sum immediately, when the excess/overpayment is due to an error on the part of the agency bank. This action is independent of recovery from the pensioner. Agency banks are requested to seek guidance from respective Pension Sanctioning Authorities regarding the process to be followed for recovery of excess pension paid to the pensioners, if any.

6. If the excess/wrong payment to the pensioner is due to errors committed by the government, banks may take up the matter with the full particulars of the cases with respective Government Department for a quick resolution of the matter. However, this must be a time bound exercise and the government authority’s acknowledgement to this effect must be kept on the bank’s record. The banks may take up such cases with government departments without reference to the Reserve Bank of India. Withdrawal of pension by old/ sick/ disabled/ incapacitated pensioners

7. In order to take care of problems/ difficulties faced by sick and disabled pensioners in withdrawal of pension / family pension from the banks, agency banks may categorize such pensioners as under: Pensioner who is too ill to sign a cheque / unable to be physically present in the bank. Pensioner who is not only unable to be physically present in the bank but also not even able to put his/her thumb impression on the cheque/ withdrawal form due to certain physical defect /incapacity.

8. With a view to enabling such old/sick/incapacitated pensioners to operate their accounts, banks may follow the procedure as under: Wherever thumb or toe impression of the old/sick pensioner is obtained, it should be identified by two independent witnesses known to the bank, one of whom should be a responsible bank official. Where the pensioner cannot even put his/her thumb/ toe impression and also would not be able to be physically present in the bank, a mark can be obtained on the cheque/withdrawal form, which should be identified by two independent witnesses, one of whom should be a responsible bank official. The responsible bank official has to be from the same bank, preferably from the same branch, where the pensioner is having his/her pension account.

9. The pensioner may also be asked to indicate to the bank as to who would withdraw the pension amount from the bank on the basis of cheque/ withdrawal form as obtained above and that person should be identified by two independent witnesses. The person who would be actually drawing the money from the bank should be asked to furnish his signature to the bank. 10. Accordingly, the agency banks are requested to instruct their branches to display the instructions issued in this regard on their notice board so that sick and disabled pensioners could make full use of these facilities. Agency Banks are also advised to strictly implement the instructions issued by RBI regarding the facilities to be provided to the sick and disabled persons and sensitise staff members in the matter and to refer to the FAQs on pension disbursement hosted on our website (www.rbi.org.in) in case of any doubt.

Life Certificate- Issuance of Acknowledgement 13. There have been complaints that life certificates submitted over the counter of pension paying branches are misplaced causing delay in payment of monthly pensions. In order to alleviate the hardships faced by pensioners, agency banks were instructed to mandatorily issue duly signed acknowledgements. They were also advised to consider entering the receipt of life certificates in their CBS and issue a system generated acknowledgement which would serve the twin purpose of acknowledgement as well as real time updation of records. Banks may provide digital acknowledgments in respect of digital life certificates submitted by the pensioners.

Pension paying banks should compensate the pensioner for delay in crediting pension/ arrears thereof at a fixed interest rate of 8 per cent per annum for the delay.

When the agency bank is calculating pension, the branch should continue to be a point of referral for the pensioner lest he/she feels disenfranchised.

All branches having pension accounts should guide and assist the pensioners in all their dealings with the bank.

Suitable arrangements should be made to place the arithmetic and other details about pension calculations on the web, to be made available to the pensioners through the net or at the branches at periodic intervals, as may be deemed necessary and sufficient advertisement is made about such arrangements.

Read more.

Home/Top

Date: April 02,2025.

Reserve Bank of India (Interest Rate on Deposits) Directions, 2025.

Excerpts:

5.1 There shall be a comprehensive policy on interest rates on deposits duly approved by the Board of Directors or any committee of the Board to which powers have been delegated.

5.2 The rates shall be uniform across all branches and for all customers and there shall be no discrimination in the matter of interest paid on the deposits, between one deposit and another of similar amount, accepted on the same date, at any of its offices.

5.3 Interest rates payable on deposits shall be strictly as per the schedule of interest rates disclosed in advance.

5.4 The commercial banks shall maintain the bulk deposit interest rate card in their Core Banking System to facilitate supervisory review.

5.5 The rates shall not be subject to negotiation between the depositors and the bank.

5.6 The interest rates offered shall be reasonable, consistent, transparent, and available for supervisory review/ scrutiny as and when required.

5.7 All transactions, involving payment of interest on deposits shall be rounded off to the nearest rupee for rupee deposits and to two decimal places for FCNR(B) deposits.

5.8 Deposits maturing on non-business working day for commercial banks.

5.8.1 If a term deposit is maturing for payment on a non-business working day, banks shall pay interest at the originally contracted rate on the original principal deposit amount for the non-business working day, intervening between the date of the maturity of the specified term of the deposit and the date of payment of the proceeds of the deposit on the succeeding working day.

5.8.2 In case of reinvestment deposits and recurring deposits, banks shall pay interest for the intervening non-business working day on the maturity value.

5.9 Deposits maturing on a Sunday/ holiday/ non-business working day for cooperative banks.

5.9.1 If a term deposit is maturing for payment on a Sunday/ holiday/ non-business working day, co-operative banks shall pay interest at the originally contracted rate on the original principal deposit amount for the Sunday/ holiday/ non-business working day, intervening between the date of the maturity of the specified term of the deposit and the date of payment of the proceeds of the deposit on the succeeding working day.